All Categories

Featured

Table of Contents

The approach has its very own advantages, but it additionally has problems with high fees, complexity, and extra, leading to it being concerned as a rip-off by some. Unlimited banking is not the most effective plan if you need just the financial investment part. The infinite financial principle rotates around using entire life insurance policy plans as a financial device.

A PUAR enables you to "overfund" your insurance policy right approximately line of it ending up being a Modified Endowment Agreement (MEC). When you make use of a PUAR, you quickly enhance your cash money value (and your death advantage), consequently boosting the power of your "bank". Better, the even more cash money worth you have, the greater your interest and dividend payments from your insurance provider will be.

With the surge of TikTok as an information-sharing system, financial recommendations and techniques have located a novel way of spreading. One such technique that has actually been making the rounds is the limitless banking idea, or IBC for brief, gathering endorsements from celebrities like rap artist Waka Flocka Fire - Whole life for Infinite Banking. While the method is currently popular, its roots trace back to the 1980s when financial expert Nelson Nash introduced it to the world.

How does Infinite Banking Wealth Strategy create financial independence?

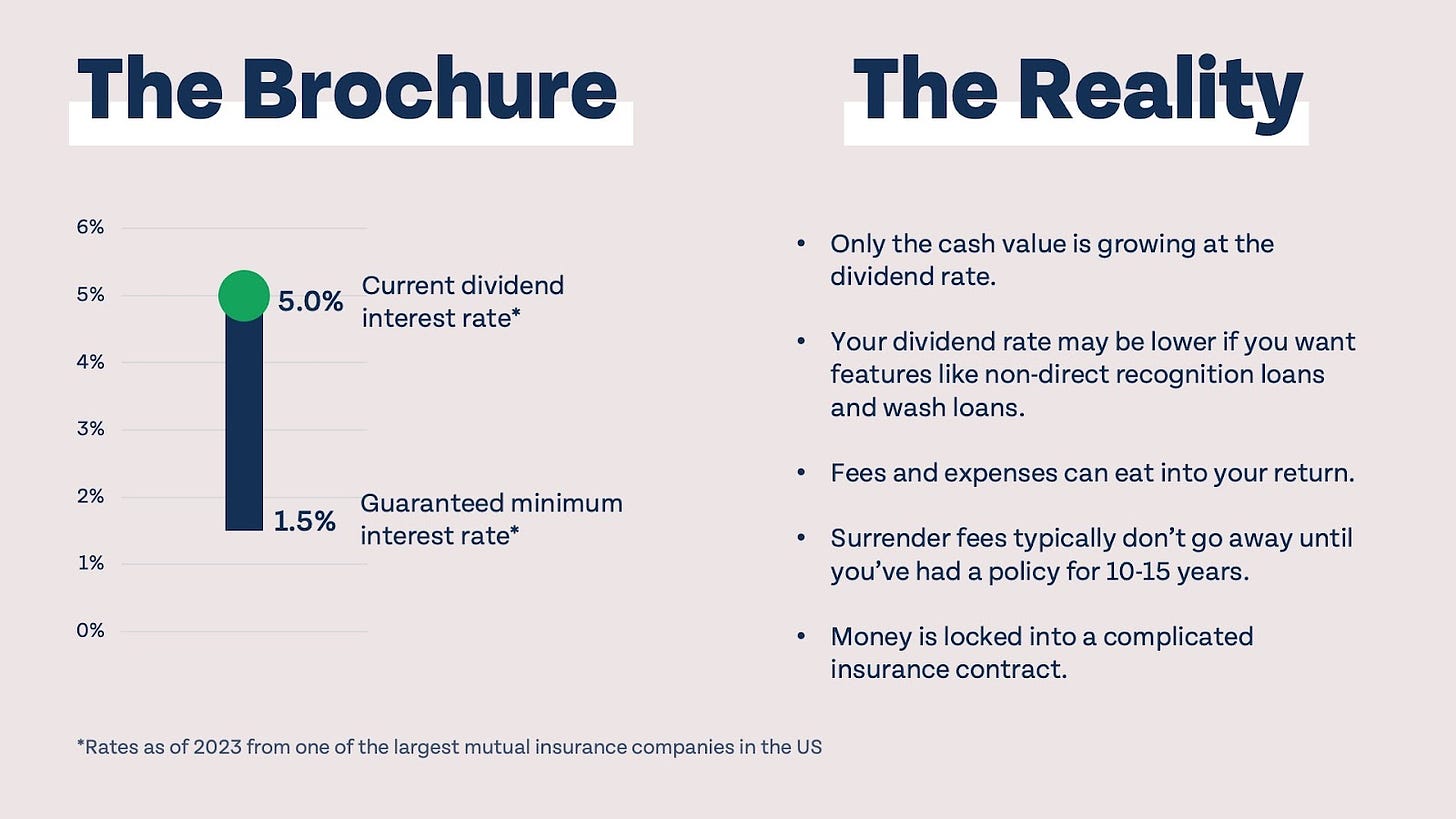

Within these plans, the money value grows based on a price established by the insurance company. Once a considerable cash money value gathers, insurance policy holders can acquire a cash money worth funding. These lendings differ from traditional ones, with life insurance policy serving as security, suggesting one can lose their coverage if borrowing exceedingly without sufficient cash money worth to sustain the insurance coverage prices.

And while the appeal of these plans appears, there are natural limitations and threats, demanding thorough cash value monitoring. The method's legitimacy isn't black and white. For high-net-worth people or entrepreneur, particularly those using approaches like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance growth might be appealing.

The attraction of unlimited banking does not negate its difficulties: Cost: The fundamental demand, an irreversible life insurance policy, is pricier than its term equivalents. Eligibility: Not everybody gets whole life insurance policy because of rigorous underwriting procedures that can leave out those with details wellness or lifestyle problems. Intricacy and danger: The intricate nature of IBC, paired with its risks, may hinder many, particularly when easier and less dangerous options are offered.

What are the benefits of using Infinite Banking Concept for personal financing?

Alloting around 10% of your regular monthly earnings to the policy is simply not possible for many individuals. Using life insurance policy as an investment and liquidity source requires self-control and surveillance of policy money worth. Seek advice from a monetary consultant to figure out if limitless banking straightens with your top priorities. Component of what you check out below is simply a reiteration of what has actually already been claimed above.

Before you obtain yourself into a scenario you're not prepared for, recognize the complying with first: Although the concept is frequently marketed as such, you're not actually taking a loan from on your own. If that held true, you would not need to settle it. Rather, you're obtaining from the insurance policy business and need to repay it with rate of interest.

Some social media blog posts recommend using cash worth from whole life insurance policy to pay down credit history card debt. When you pay back the lending, a section of that passion goes to the insurance business.

What do I need to get started with Borrowing Against Cash Value?

For the very first several years, you'll be paying off the compensation. This makes it exceptionally tough for your policy to accumulate value during this time. Unless you can afford to pay a few to numerous hundred bucks for the following decade or more, IBC won't work for you.

Not everybody needs to rely exclusively on themselves for monetary protection. Wealth management with Infinite Banking. If you need life insurance policy, below are some useful ideas to consider: Consider term life insurance policy. These policies offer coverage during years with considerable financial responsibilities, like home mortgages, trainee loans, or when caring for little ones. Ensure to look around for the very best price.

What are the common mistakes people make with Leverage Life Insurance?

Visualize never having to stress regarding bank finances or high interest rates once again. That's the power of unlimited financial life insurance policy.

There's no collection loan term, and you have the flexibility to choose the repayment schedule, which can be as leisurely as repaying the lending at the time of death. This flexibility expands to the maintenance of the financings, where you can go with interest-only settlements, keeping the car loan equilibrium level and workable.

How secure is my money with Wealth Management With Infinite Banking?

Holding money in an IUL repaired account being attributed rate of interest can usually be much better than holding the money on deposit at a bank.: You've constantly desired for opening your own bakeshop. You can obtain from your IUL plan to cover the first costs of leasing an area, acquiring equipment, and working with staff.

Personal car loans can be gotten from typical banks and credit rating unions. Obtaining money on a credit rating card is usually very expensive with yearly percent rates of rate of interest (APR) usually reaching 20% to 30% or even more a year.

{kind=link}

Latest Posts

How To Become My Own Bank

Whole Life Insurance Bank On Yourself

Infinite Banking Canada